The former started confidently, dominating the field. But at the end of February, the latter stormed out and for a while seemed to be gaining the upper hand. At half-time, both teams have scored but neither has the upper hand. The most likely scenario for the second half is a gradual strengthening of the Capex team, whilst the Energy Shock team would continue to hold the field and influence the game, without however managing to gain the upper hand, before letting victory slip away as 2027 approaches.

Team overview

On the Capex side, we are dealing with a global investment cycle driven by four key factors:

- Defence, fueled by a shake-up of the global geopolitical order requiring most countries to step up significantly their efforts in this area;

- Artificial intelligence (AI), the driving force behind a new gold rush involving colossal investments in digital infrastructure;

- Energy generation, fueled both by the needs of the energy transition and the voracious demand for electricity from data centres, which are essential to the development of AI;

- Supply chains resilience to geopolitical, geo-economic, climatic and pandemic disruptions, which seem to have become the new norm since 2020.

On the ‘Shock’ side, the near-total closure of the Strait of Hormuz for four months – preventing around 20% of the world’s fossil fuel supply from leaving the region – caused the biggest energy supply disruption in history in quantitative terms. Fortunately, the impact on prices was much more moderate – peaking at around +63% for oil and +88% for gas consumed in Europe. This was achieved thanks to an unprecedented mobilisation of strategic reserves by OECD countries and China’s unilateral decision to halve its crude oil imports[1].

Developments in the first half

The memorandum of understanding signed on 17 June between the United States and Iran has, over recent weeks, kicked off a gradual return to normal for the transit of oil and gas tankers through the Strait of Hormuz. Oil prices have fallen back to their pre-war levels, whilst European gas prices remain around 43% higher. The energy crisis has lost momentum.

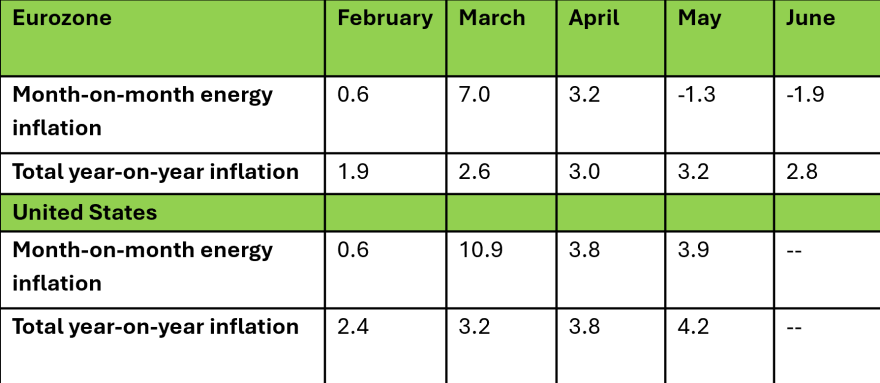

Nevertheless, it has led to a sharp rise in inflation, driven by soaring energy prices (see table); a reversal of expectations regarding monetary policy easing by the major central banks; and, in the case of the ECB, a 25-basis-point rate rise in June.

The Fed and the Bank of England have held off so far, but the markets are now anticipating a tightening of policy rather than the multiple rate cuts forecast before the war. This has contributed to a sharp rise in long-term bond yields (of nearly 30 basis points for 10-year German government bonds and more than 50 basis points for equivalent bonds issued by France, the United Kingdom or the United States). Added to this is weaker-than-expected growth in the first quarter in most countries, and composite business confidence indices in contractionary territory or, at the very least, in sharp decline in the second quarter in most cases.

Against this backdrop, the Capex team also scored: business sentiment indices in the manufacturing sector remained in expansionary territory across all G7 countries and, everywhere except Germany, were higher in June than before the war. Furthermore, business sentiment in the services sector began to pick up in June (except in the United Kingdom). Unemployment rates remained at historically low levels. Finally, stock markets are generally well above their pre-war levels, with double-digit gains in tech-heavy markets such as the US Nasdaq and the Japanese Nikkei.

Outlook and key points to watch in the second half

Our baseline scenario anticipates robust growth between now and the end of the year, but not enough to offset the slowdown caused by the energy shock. More specifically, we expect US growth to average 2.4% in 2026, growth in the eurozone (excluding Ireland) to reach 1%, and growth in Germany, France and Italy to be 0.8%. This is lower than expected before the war, but better than in 2025, except for the eurozone and France. Inflation, too, unfortunately, is expected to remain relatively robust at around its current level until the end of the year, before falling in 2027. This is why we anticipate at least one rate rise by the Fed (followed by others next year), and likely one by the BoE and the ECB as well[2].

A more favourable scenario is possible: if oil supply rises significantly faster than demand, the market could find itself in a substantial surplus and prices could fall further. In Europe, the major public investment efforts underway in Germany could further accelerate[3] and, thanks to the structural reforms announced last week, finally begin to trigger a surge in private investment. The recent rebound in household confidence could lead to a faster normalisation of consumption.

Nevertheless, there is no shortage of downside risks either. Even if pressure on energy prices eases sustainably, we are not immune to a new supply shock arising from ongoing climate disruption, or to the exploitation of other bottlenecks in global supply chains.

As for the investment cycle, AI clearly dominates; however, projects totaling more than USD 1,000 billion by US tech giants could come to an abrupt halt should their highly ambitious return forecasts be revised downwards. The shockwave across financial markets would be profound, and would not be confined to them, as the real economy – deprived of this star player – would also be affected. Finally, let us not forget geopolitics, notably the mid-term elections in the United States and the approaching presidential election in France, which are likely to create further uncertainty.

With all this to play for, the end of the game is unlikely to be a dull affair.

[1] See our EcoFlash on this topic – Reopening of the strait of Hormuz: The oil market between short-term relief and persisting uncertainties, 16 June 2026

[2] To explore this scenario in greater detail, don’t miss our editorial – U.S.- Iran memorandum of understanding: to what extent has it improved the economic outlook? (22 June 2026) and our Scenarios and Forecasts.

[3] For an update on this plan, read our EcoFlash ‘German investment plans: reasons to stay optimistic’, 25 June 2026.